The important question is How Much Should I Save to Buy a House? However, Investing in a future home is a great way to accumulate cash and create a more comfortable feeling. Knowing the numbers can help you set a sensible savings goal so that your future home becomes an asset rather than a liability.

In 2024, the rising costs of rising mortgage rates and skyrocketing prices could weigh heavily on first-time homebuyers. Even though thinking about money can be frustrating, buying a home is a wise choice for building a solid financial future. It is important to understand the essential expenses involved in achieving homeownership.

Key Factors to Consider

1-How much money do you need for a down payment?

Increasing the down payment can reduce the amount borrowed, resulting in cheaper monthly payments. A down payment is the first amount you pay to purchase a home. Lenders prefer higher down payments because they indicate a lower risk of default in case the loan is not repaid.

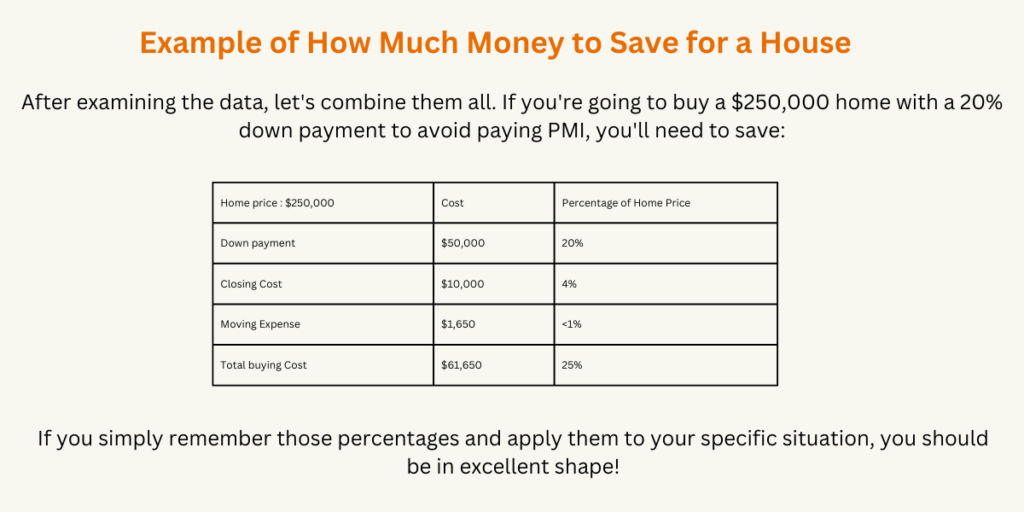

A down payment of at least 20% is recommended to avoid paying private mortgage insurance (PMI), an annual fee that amounts to approximately 1% of your loan balance. This saves you big money and means lower monthly payments and less debt. First-time home buyers should make a 5-10% down payment, but be prepared to pay for PMI. Less than 5% down payment is bad, as it will result in higher monthly payments.

Make sure you can afford a home by paying 25% of your take-home pay monthly, including taxes, homeowner’s insurance, and HOA fees. Overspending can limit your budget and save for retirement. A 30-year mortgage can result in additional interest and debt for an additional decade and a half, so choosing a mortgage that fits your budget and needs is important.

Additionally, if you are currently in debt, you should not start saving for a house or buying one as this will only create bigger problems. If you pay off your debt and eliminate all those monthly payments first, it won’t take you as long to save up a big down payment.

Advice on making a down payment fund

That big down payment when buying a home requires work, no matter how much you intend to invest. Keep the following things in mind when saving money for your down payment:

- Explore local assistance programs for first-time homebuyers.

- Consider grants or zero-interest loans for down payment costs if eligible.

- Cut back on expenses like cable, cell phone service, and eating out.

- Use savings from CDs in high-yield savings accounts.

- Compare interest rates on money storage options.

- Seek help from relatives or friends who can provide the down payment.

- Submit a gift letter confirming that the loan is a gift and not a loan.

2-How much money do you need for closing costs?

The expenses you pay for services that help formally close the sale of a property are called closing costs. Closing fees for buyers typically include:

- home inspection

- Evaluation

- initial cost

- title insurance

- Homeowners Insurance

- taxes

If you’re wondering how much all that stuff costs, an appraisal typically costs around $360, and a home inspection costs around $340 on average.2,3 Sadly, others on the list The prices of goods will be quite high.

Adding it all together, your closing fees will likely be between three to four percent of the home’s sales price. This is the amount you should be prepared to pay.

Is it possible to avoid closing costs?

Closing fees are inevitable, but you can avoid paying them all at once. Additionally, in a buyer’s market, you may be able to negotiate at least some of the closing fee. Inquire with your lender about options that waive closing costs if finding the funds to cover them seems impossible. Some lenders will include the cost in the total loan amount. Just remember that since you’ll be paying interest on the extra cash, doing so will cost you more in the long run.

You should also set aside money for any additional costs you may incur when moving into your new home, such as storage fees, furniture, repairs, and closing fees.

3-Prepaid expenses

Apart from the closing fees, prepaid expenses will also have to be paid. These are lump sum cash payments made at closing for specific mortgage costs, such as homeowners insurance, property taxes, and mortgage interest, that you pay before they are actually due. Your lender will likely hold your money in escrow for these regular monthly fees until the loan is paid off.

earnest money deposit

Additionally, potential buyers show that they are serious about buying a home by putting down a down payment. Typically, 1% of the agreed purchase price of the home must be paid. However, the earnest money deposit only represents a portion of your upfront cost; This is not an extra expense. Once your offer is accepted, you make the deposit within a day or two, and it is applied to your closing costs.

store of wealth

Additionally, your lender will check to see if you have enough saved to pay off your mortgage in the event of an emergency or a change in your income. Months are used to measure mortgage reserves. For example, if after you close on your home, you have $7,200 in your savings account and your monthly home loan payment is $1,200, you have six months of reserves. Generally speaking, illiquid assets – such as money that can only be withdrawn after retirement – are not counted as reserves.

- Explore more about The idea of the 80-20 rule.

4-How much cash is needed for relocation-related costs?

Now, you have amazing friends and if you can buy enough pizza for your friends and family to help you get away with all your stuff for free, you can skip this step! However, if not, you’ll probably have to pay for some moving expenses. Although transfer fees aren’t as expensive as the other costs we’ve discussed, you won’t be able to pay them with money hidden under your sofa cushions.

How you want to make your move will determine how much you’ll have to pay in moving expenses. If you decide to use movers, budget for around $1,700. However, if you choose to do it yourself and rent a moving truck and pack your belongings yourself, the costs will be lower.

local vs out of state

Remember that while local moving can be expensive, cross-country or out-of-state moving is even more expensive. Long-distance travel also incurs additional costs when you travel from one place to another, such as lodging, gas, or flights.

5-Housing payment

It’s important to consider when estimating how much money you’ll need to purchase a home, not just on closing day, but how much you’ll need each month.

One of the most predictable recurring expenses is your mortgage payment every month. The mortgage calculator at Bankrate can be used to determine your monthly payment amount. For example, if you borrowed $240,000 and financed it with a 30-year, fixed-rate mortgage at 6.0 percent, you would pay $1,438 in principal and interest each month.

What’s the best way to get the cheapest fare?

Finding the best mortgage rate requires comparison shopping between lenders as it significantly impacts your monthly mortgage payment. For example, if you took out the same $240,000 loan at a rate of 7.0 percent, your monthly principal and interest payment would be $1,596.

More than 75% of all borrowers applied for a mortgage with only one lender, the Consumer Financial Protection Bureau reports. During a loan, failing to comparison shop could cost you hundreds of dollars.

6-Ongoing expenses associated with homeownership

In addition to your monthly mortgage payment, there are other expenses associated with becoming a homeowner. Aim to set aside at least 1% of your annual property value as a budget item for urgent repairs and maintenance. For example, you’d budget $3,000 per year for maintenance-related expenses on a $300,000 home.

If your property is part of an association, don’t forget to account for homeowner’s insurance, property taxes, HOA dues, utility bills, and ongoing maintenance costs.

Preparing to buy a house

After determining how much money you need to purchase a home, it’s time to prepare for the actual purchase. Here are the main steps to get ready:

check your credit

Mortgage lenders assess your credit score to determine your creditworthiness. Get your credit score from the three major credit reporting agencies, an online service, or your bank. If your score is low, work on improving it before applying for a mortgage.

Review all of your expenses to establish a realistic budget. Many experts suggest following the 28/36 percent rule: spend no more than 28 percent of your gross monthly income on housing and no more than 36 percent on total debt.

Save for a down payment

You typically need at least 3 percent of the home’s purchase price as a down payment. To avoid mortgage insurance, aim for a down payment of at least 20 percent.

shop for lender

Getting pre-approved by a lender shows sellers that you are a serious buyer and helps you understand how much home you can afford. Compare quotes from at least three lenders to find the best deal.

be willing to compromise

With rising home prices, you may have to compromise on some amenities like a garage or finished basement. Remember, you can always make improvements and upgrades after purchasing a property.

By following these steps, you will be well prepared to move forward in the home-buying process and make an informed decision.

What should you do next?

The best thing to do now is to get a top level real estate agent on your side, another thing you can do to ensure that once you have deposited the appropriate amount and are ready to buy the house. If you are prepared, you are well prepared.

- Work with a local real estate agent.

- Get referrals from family and friends.

- Interview several professionals before choosing a Realtor.

- Compare rate offers from at least three lenders.

- Create a budget accounting for both upfront and ongoing expenses.

- Monitor monthly finances to ensure that the mortgage and ongoing expenses will not be a long-term financial burden.

For now, I hope this article has helped you understand How Much Should I Save to Buy a House?

Have you ever wondered how Adidas founder Adolf Dassler made his fortune from one idea Check out The Untold Story of Adolf Dassler’s Creative Legacy, plus more in my Startup section.